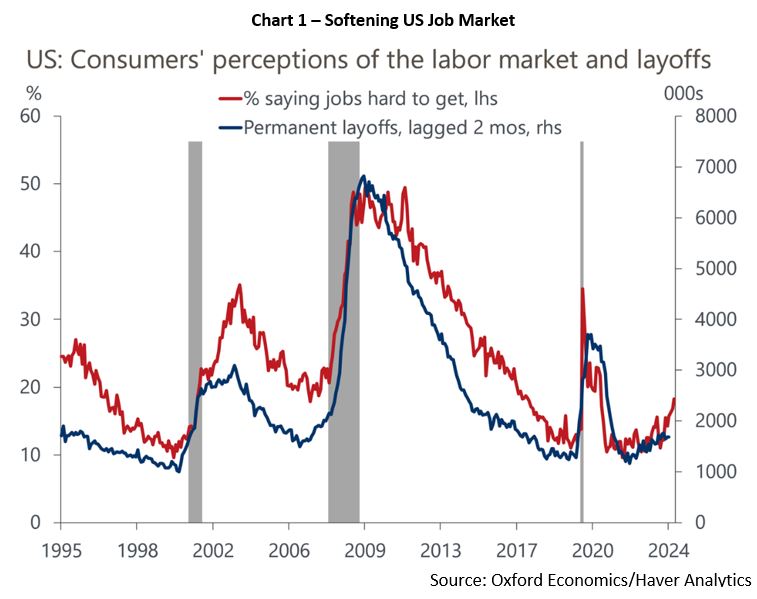

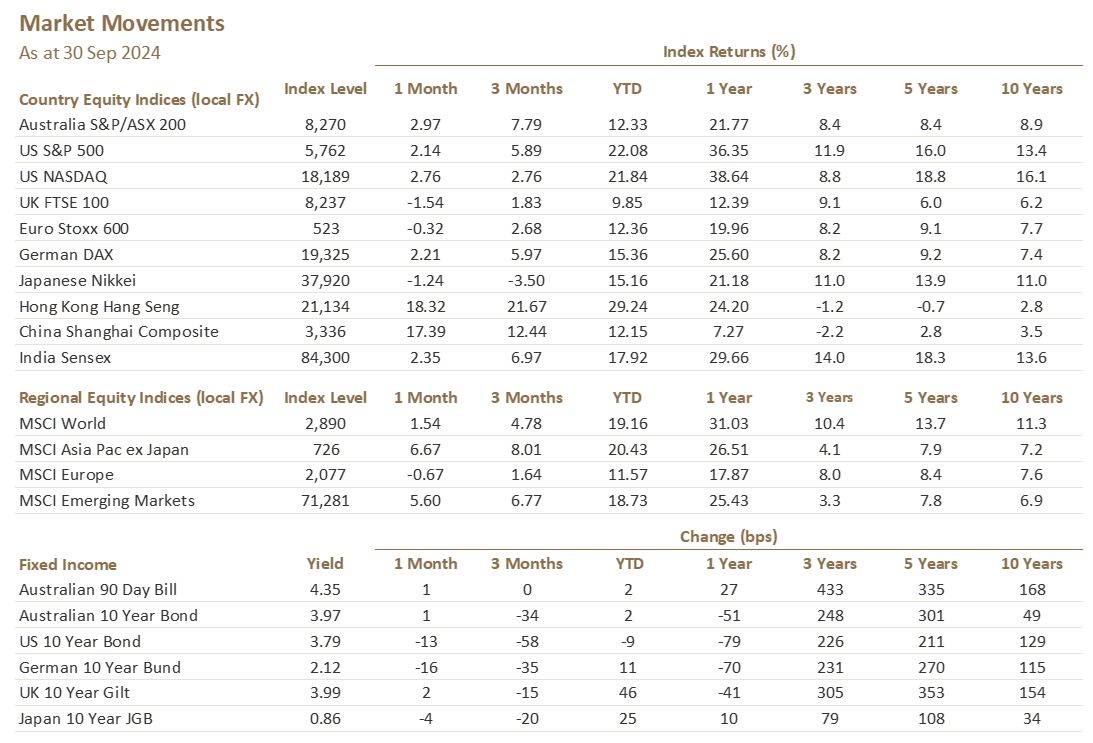

US stocks leaped to record highs after the Federal Reserve (Fed) delivered a higher-than-expected interest rate cut of 50 basis points to 4.75-5.0% at the September FOMC meeting. Signalling the beginning of a new monetary easing cycle against the current disinflationary backdrop, the US S&P 500 ended 2.14% higher in September. Core inflation was revised downward by 0.2% this year to 2.6% and continues to taper to 2% by 2026. J.P. Morgan Research expects the Fed to cut rates by another 50 basis points at its next meeting in early November, though this is contingent on further softening in the two jobs reports between now and then. Chart 1 shows this softening through time and layoffs have started to inch higher, prompting the Fed to act now to preserve a strong labour market and help the economy return to a favourable place over time.

While other global central banks including the European Central Bank, Swiss National Bank and Bank of Canada have begun easing their monetary policy stance, the Reserve Bank of Australia (RBA) held the cash rate steady at 4.35%, maintaining their hawkish stance. Governor Michele Bullock said the board did not actively consider raising rates but did discuss whether or not its hawkish messaging should change at the September meeting. She reiterated policy would have to be sufficiently restrictive to ensure inflation returns to target and does not bounce in and out of the 2-3% range but remains firmly in the band. Major developed countries have shown a steady fall in inflation which is very positive to begin the easing cycle and encourage activity (Chart 2). This is particularly important as the JPM Global manufacturing PMI declined at an accelerating pace in September (49.6 to 48.8) followed by deteriorating international trade flows and falling business confidence.

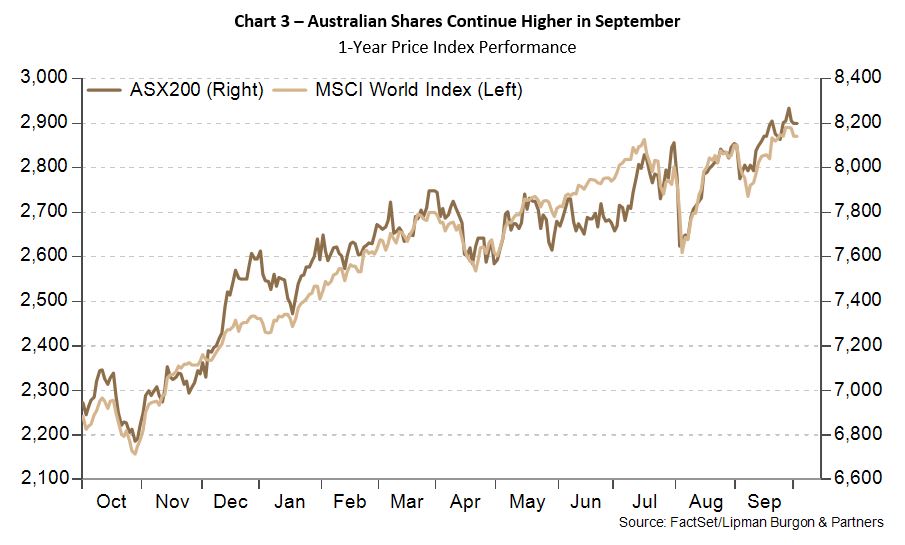

Despite the RBA’s hawkish tone, investor sentiment has taken a leg up in recent weeks with the Fed rate cut, pushing the ASX200 up almost 3% in September (Chart 3). This equity market growth was further bolstered by strengthening of the Australian Dollar to US69c as the Fed began its expansionary stance, and on the announcing of China’s fiscal support to revive its economic prospects. The soft landing case may come to fruition as central banks generally cut rates for one of two reasons; because economic growth is faltering such as during the financial crisis in 2008, or because higher rates have successfully brought down inflation and the bank can recalibrate its policy. Inflation has continued to subside, and these rate cuts will help support the US economy to maintain its low unemployment. This may also be a positive for equities as they generally benefit from lower interest rates.

China’s Stimulus Measures to Boost Faltering Economy

The People’s Bank of China (PBOC) unveiled its biggest stimulus since the pandemic to pull the economy out of its deflationary funk and given how depressed Chinese share prices have become; it won’t take much for them to outperform global and emerging market equities for a few months. In September alone, the Shanghai Composite surged over 17%. The PBOC cut interest rates on existing mortgages by 0.5% and supported new lending by reducing the level of reserves banks must set aside before making loans. The bank’s governor, Pan Gongsheng, said he would also ease restrictions on borrowing to invest in stocks and shares on Chinese exchanges and reduce the deposit needed to buy a second home from 25% to 15%. The central bank expects this to help about 50 million households, reducing the total interest bill by about 150bn Yuan (AUD31bn) a year. Beijing is aiming for an economic growth target of about 5% for 2024 while Goldman Sachs, UBS and Bank of America have recently lowered their forecasts. The goal of this stimulus package is to boost business and consumer confidence; while promoting growth, particularly as real lending rates remain high (Chart 4) and the effects of deflation persist.

Portfolio Positioning

As always, while it is important to keep on top of global economic and political news, one should refrain from reacting too quickly in their portfolio, particularly with a long term investment horizon (10+ years). There may be some cases however, where trimming certain asset class exposures when they have reached elevated valuations is the optimal portfolio tilt.

As we enter into the last quarter of 2024, the LBP Investment Committee will consider and discuss the current economic landscape we are in, to determine portfolio positioning for the next 3 months. In these meetings, we consider our strategic asset allocation, our capital return and income targets, as well as the most optimal way to gain exposure to a multitude of factors. Diversifying factor exposures ensures your portfolio is insulated from drawdowns in specific asset classes such as bonds, equities or real estate, and enables it to perform more robustly.

Our investment philosophy is one that focuses on the long-term wealth goals of capital preservation and income generation, and we do this through a disciplined investing framework and remaining invested through the cycle. As evidence shows that timing the market often leads to sub-optimal outcomes, we focus on creating robust multi-asset class portfolios with diversified risk factors.

We encourage you to contact us should you wish to discuss this further or if you have any questions about how these trends are impacting your portfolio.

This article has been prepared by Lipman Burgon & Partners AFSL No. 234972 for information purposes only; is not a recommendation or endorsement to acquire any interest in a financial product and, does not otherwise constitute advice. By its nature, it does not take your personal objectives, financial situation or needs into account. While we use all reasonable attempts to ensure its accuracy and completeness, to the extent permitted by law, we make no warranty regarding this information. The information is subject to change without notice and all content is subject to the website terms of use.

Recent Comments